By Enrico Sieni·Revify Analytics·2026-06-24·~13 min read

Marginal price is the price you set on the next unit or the next deal. Think of the spot order for extra volume, or the add-on line a seller drops onto a quote, or the repeat buyer asking for one more truckload at the usual favor. Each decision is small, which is exactly why it gets made on instinct. Add up a quarter of those instincts and you have the real reason a healthy-looking margin drains away. It is also the fastest place a mid-market manufacturer or distributor can recover profit without standing up a pricing team.

Table of Contents

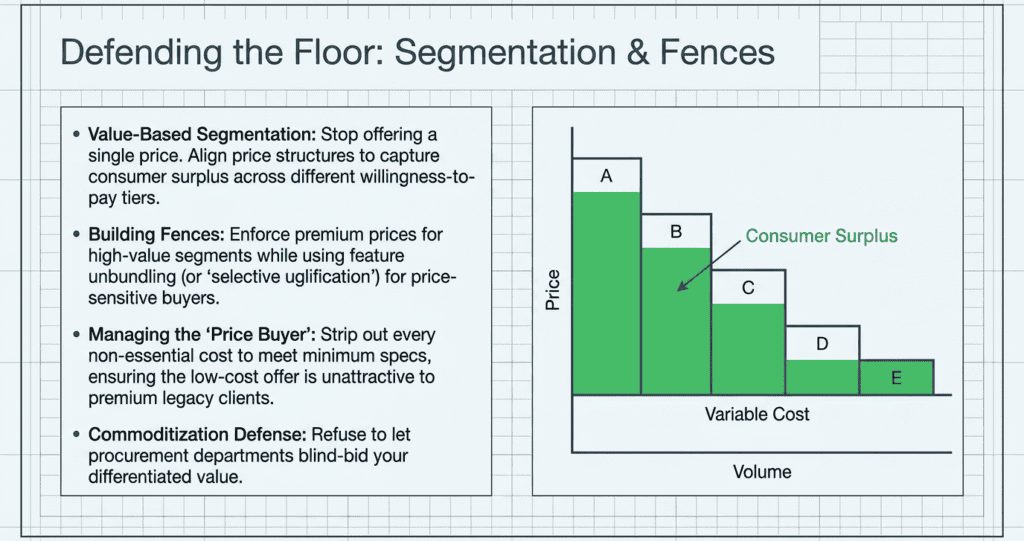

What does marginal price actually mean?

On a cost sheet, marginal refers to one additional unit. In sales, the marginal price is the amount a seller charges for an additional unit or order. Economics textbooks explain this as the intersection of marginal revenue and marginal cost, where profit is maximized. While accurate, this is not how a regional sales manager approaches a real-time negotiation. In practice, they decide how far below the list price they are willing to go to secure incremental volume.

How it differs from list price, pocket price, and marginal cost

List price is the published amount before negotiation. Pocket price is what remains after all discounts, rebates, and freight concessions. Marginal cost is the expense of producing or sourcing the next unit. Marginal price falls between these figures. It is the quoted price for an incremental deal, and the profit is the difference between this price and the marginal cost, minus the cost to serve. The most damaging mistake is treating marginal cost as marginal price. Cost sets the minimum, but does not determine the appropriate price.

Why does the term confuse commercial teams?

Finance often interprets ‘marginal’ as marginal cost, while sales may view a marginal deal as insignificant. Both perspectives can lead to unnecessary price concessions. Even small deals at low marginal prices affect overall margin, and repeated concessions have a significant impact. This confusion is practical, not theoretical, and often results in discounts that would not be approved in a formal pricing review.

Why does marginal price matter more than chasing volume?

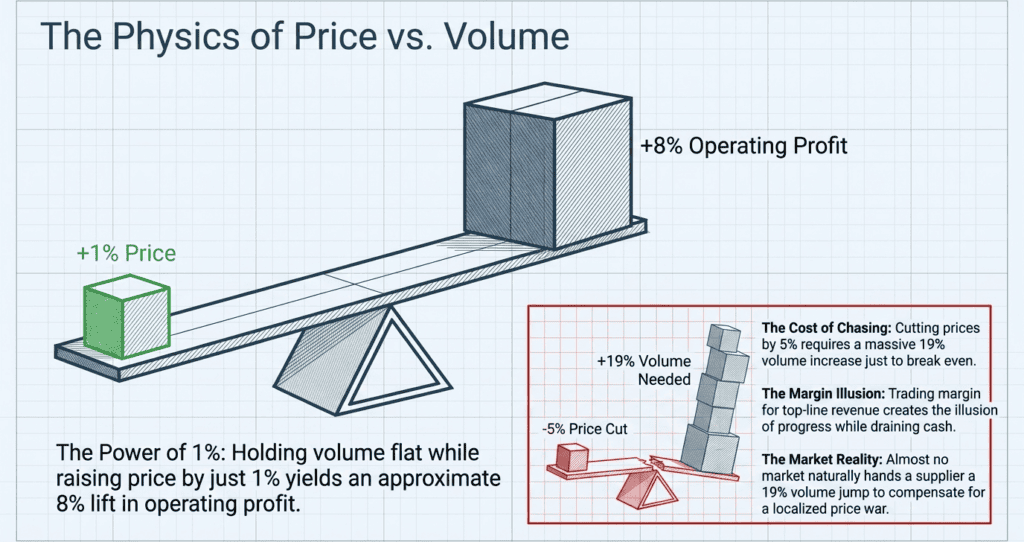

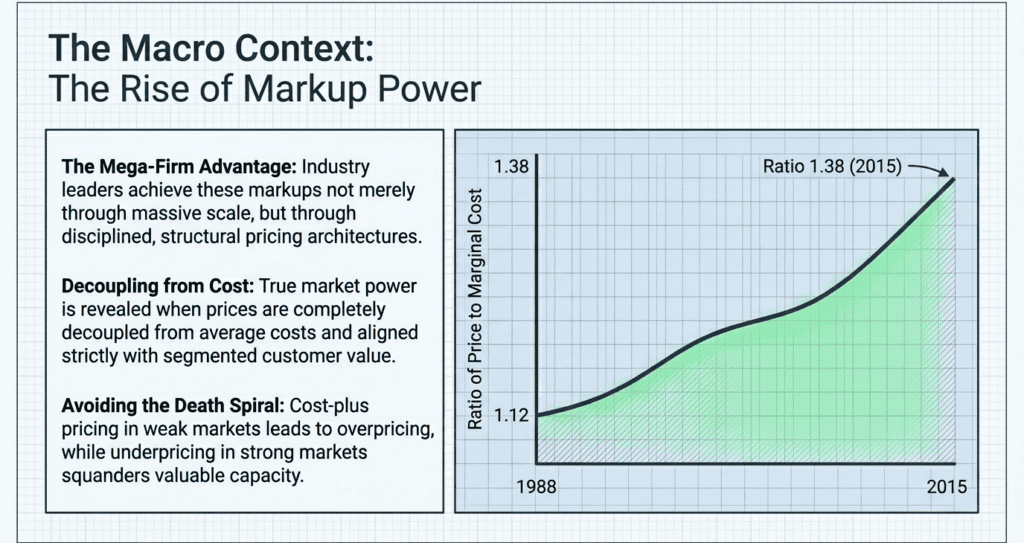

Price is the most sensitive lever on the income statement, and the marginal deals are where that lever actually gets pulled. McKinsey’s long-running analysis of pricing puts a number on it: for a typical S&P 1500 company, raising price by one percent while holding volume lifts operating profit by roughly eight percent. You can read their write-up in The Power of Pricing. The phrase “while holding volume” carries weight, and a sophisticated reader will catch it. The exact impact varies by industry, margin structure, and customer price sensitivity. The directional lesson holds regardless: price moves profit harder than almost anything else in the statement. The arithmetic also runs in reverse. Shave a few points off enough marginal prices, and the profit line falls faster than the revenue line, because price drops straight to the bottom while volume drags cost along with it. McKinsey’s own figure is blunt about cuts: to recoup the profit lost from a five percent price reduction, volume would have to climb almost nineteen percent. Almost no market hands you that.

Focusing on marginal price is more effective than pursuing volume alone. Securing incremental volume at prices that do not cover true costs sacrifices margin for revenue, resulting in apparent growth without real profit. Companies that protect their margins consistently identify their marginal price floor for each deal and avoid going below it without justification.

Where does the marginal price break down in mid-market manufacturing?

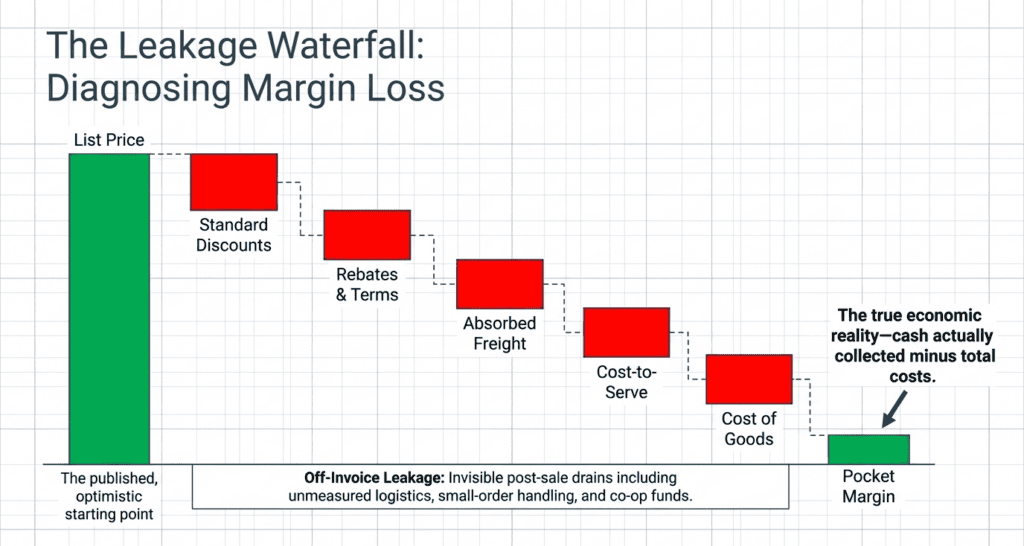

In most mid-market manufacturers and distributors, nobody sets out to give away margin. It leaks through the incremental decisions, one reasonable-sounding concession at a time. This is the world of transaction pricing, where the price of each individual deal, not the published list, decides the margin.

We walk through the mechanics in our guide to eliminating margin leakage, and the short version is that the damage is rarely on the invoice. It is in the pocket.

When incremental pricing happens without guardrails

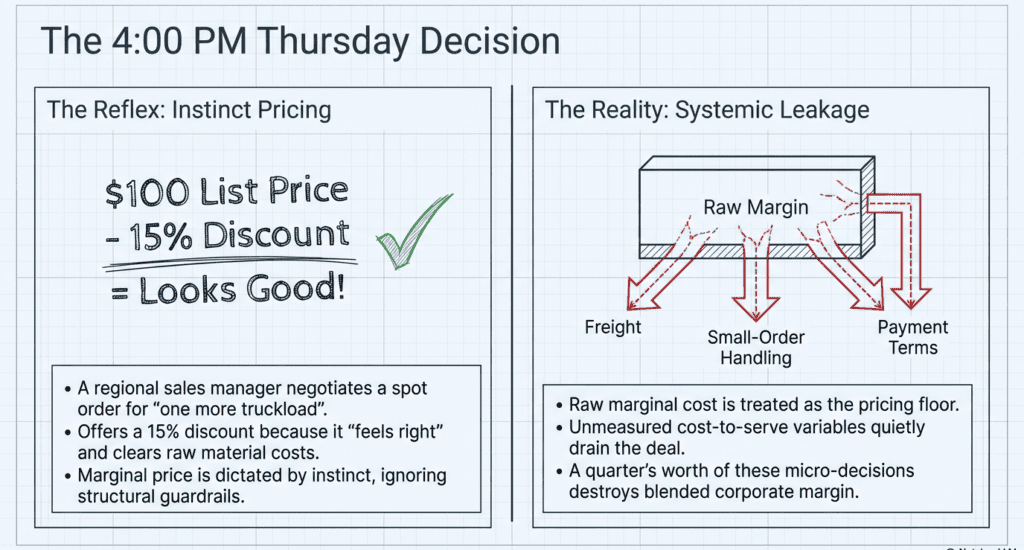

Incremental pricing involves setting a price for each new order rather than for the entire customer relationship. With proper controls, it enables profitable spot business. Without controls, it encourages a race to the lowest price, as previous discounts set new expectations. When sellers do not document the reasons for concessions, these discounts become routine rather than deliberate decisions.

How exceptions, discounts, and freight erode the gain

Three main factors erode margin: off-invoice discounts, which are not visible in list-to-net comparisons; freight costs, often absorbed to close deals and rarely recovered; and small orders, where handling costs can outweigh the margin. These issues may seem minor individually, but collectively they cut pocket margin by several points. A deal that appears profitable at the marginal price may result in an unacceptable pocket margin if these factors are not considered.

What is the marginal cost formula, and how does it set the floor?

To establish a marginal price floor, you must first determine where that floor lies. This begins with calculating marginal cost.

Marginal cost, written MC, is the change in total cost divided by the change in quantity: MC = ΔTC / ΔQ. It answers one question. What did the next unit cost me? Marginal revenue, MR, is the matching idea on the revenue side, the change in total revenue from selling one more unit. The textbook rule is to keep selling while MR sits at or above MC, with profit peaking where the two meet.

The marginal cost formula sets a firm’s minimum; selling below this point results in a loss on every unit sold. However, this minimum is not the same as the appropriate price. A marginal price that only covers marginal cost overlooks additional costs to serve, such as freight, handling, payment terms, and returns. A more accurate minimum requires that the marginal price cover the marginal cost, the cost to serve, and the desired incremental margin. Pricing below this threshold may appear profitable, but it ultimately erodes margin. This is the risk of pricing based solely on cost.

Costs do not sit still either. When input costs jump, the floor moves with them, and a marginal price set on last year’s cost is suddenly underwater. We have written about holding the line on industrial margins when costs move against you, and a stale threshold is one of the first places that pressure shows up.

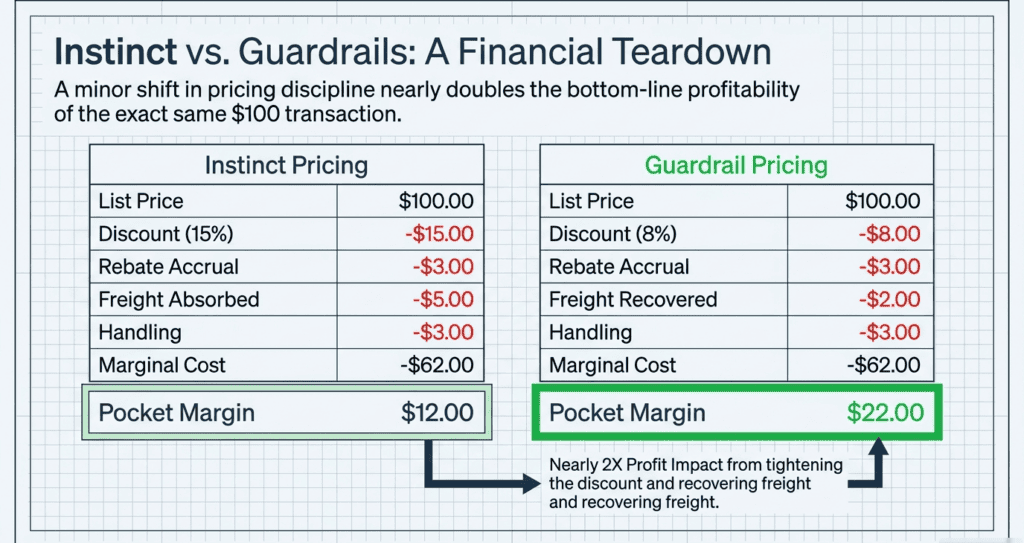

Here is what the minimum looks like on a single incremental order. A distributor gets a spot request for extra volume from a known account. The list price is $100 per unit. The seller wants to win and offers fifteen percent off. On paper, it clears the cost. Watch what is left after the rest of the waterfall, and compare it to the same order quoted against a floor.

Waterfall step

Instinct price

Guardrail price

List price

$100.00

$100.00

Discount

-$15.00

-$8.00

Invoice price

$85.00

$92.00

Rebate accrual

-$3.00

-$3.00

Freight absorbed

-$5.00

-$2.00

Small-order handling

-$3.00

-$3.00

Marginal (variable) cost

-$62.00

-$62.00

Pocket margin

$12.00

$22.00

These figures are illustrative, not actual client data. The only variable is whether the marginal price was set using a guardrail or simply to close the deal. The disciplined approach recovers freight costs and reduces unnecessary discounts, nearly doubling the pocket margin.

Why do two customers at the same marginal price earn different profits?

Cost to serve is only part of the equation; customer profitability over the full year is equally important. Two customers may purchase the same product at the same marginal price but generate very different profits. One may order in bulk, pay promptly, and require little support, while another may place frequent small orders, request extended payment terms, return products, and require ongoing support. The marginal price is the same, but the underlying economics differ.

This disparity can determine which deals are truly valuable. According to Harvard’s Robert Kaplan and V.G. Narayanan, the top twenty percent of customers in a typical portfolio generate between 150 and 300 percent of total profit, while the middle group breaks even, and the least profitable accounts offset much of the gain. Cost-to-serve analysis translates these insights into actionable pricing. Without visibility into deal-level and customer-level profitability, marginal prices may be set without understanding which accounts contribute most to profit.

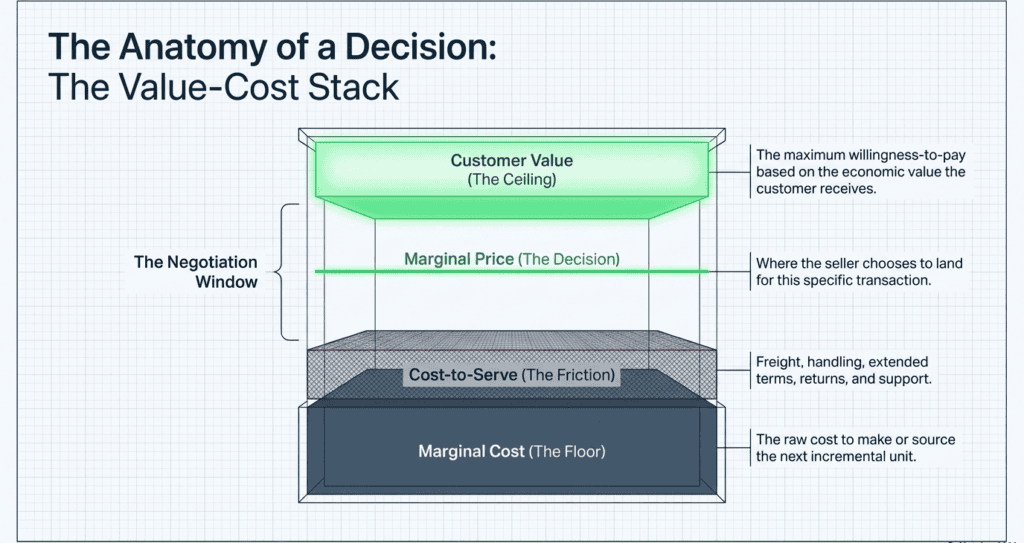

When setting a price, consider the entire value chain, from underlying costs to the value delivered to the customer.

Layer

What it is

Customer value (the ceiling)

The most the buyer will pay for the value they get

Marginal price

Where you choose to land on this deal

Cost to serve

Freight, handling, terms, returns, and support for the deal

Marginal cost (the floor)

What the next unit costs to make or source

Cost establishes the minimum price, while value determines the maximum. The key considerations for marginal pricing occur between these two points.

When should you intentionally price near marginal cost?

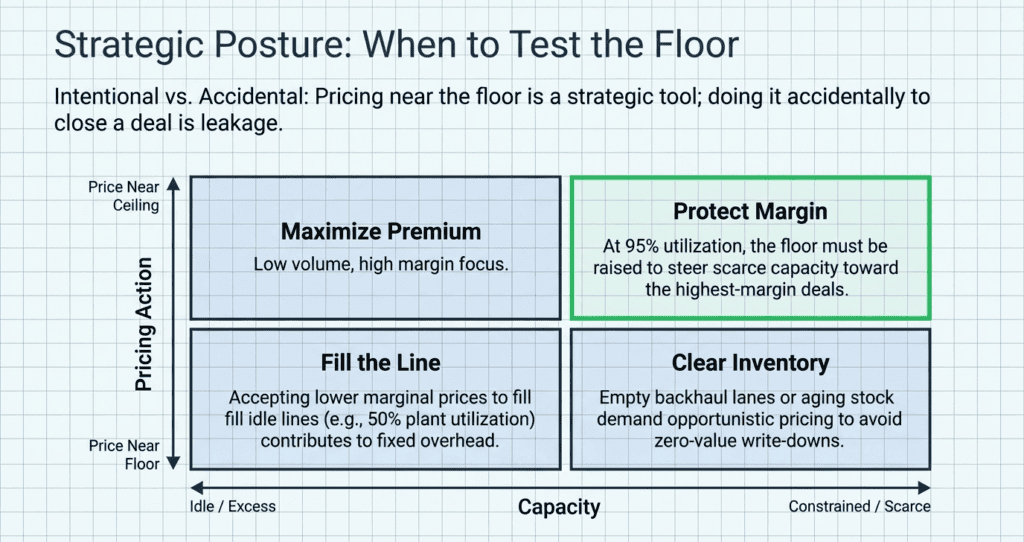

While maintaining a price floor is important, there are valid reasons to price near marginal cost. Marginal pricing is a strategic tool when used intentionally. The distinction between disciplined pricing and margin leakage lies in making deliberate, informed choices.

Several scenarios justify a low marginal price. Excess capacity is a primary example; when a facility operates below capacity, incremental orders priced just above marginal cost help cover fixed expenses and generate positive contribution margin. Perishable capacity, such as empty backhaul lanes or idle shifts, also benefits from accepting nearly any paying order. A strategically important new customer may warrant a low initial price if the long-term value is sufficient. Additionally, selling excess or aging inventory before it requires a write-down is a deliberate, opportunistic strategy.

Capacity utilization is often the key factor in marginal pricing decisions, and its implications vary depending on the business context.

Capacity situation

Marginal price posture

Plant running near 50% utilization

Accept a lower marginal price to fill the line

Plant running near 95% utilization

Hold a higher marginal price; capacity is scarce

Hard capacity constraint

Protect price hard and steer capacity to the best margin

Excess or aging inventory

Opportunistic marginal price to clear it before write-down

Demand response sets the other boundary. A marginal price should reflect not just cost but how sensitive the buyer is to price. A customer with low price sensitivity and few alternatives can support a higher marginal price than one running a competitive bid with three suppliers. This is where price elasticity and willingness to pay enter the decision. McKinsey’s pricing work is blunt about the cost of ignoring it: companies that do not price to willingness to pay tend to either price too low and leave money on the table or price too high and lose the customer. The argument is laid out in Turning Pricing Power into Profit.

The distinction is clear: a low marginal price set intentionally, for a specific reason and with a defined end date, is a strategic decision. The same price offered without oversight or justification constitutes margin leakage. The following guidance will help differentiate between the two.

What changes when you install pricing discipline?

Pricing discipline does not require extensive documentation. It means that sellers have a clear price floor, a streamlined process for exception approvals, and a consistent margin definition aligned with finance. Many mid-market teams lack at least one of these elements.

Approval rules for low-volume and incremental deals

Establish a marginal price floor by segment or product family, allowing sellers to quote freely above it. Deals priced below this minimum require additional approval. This approach balances speed with control. Most incremental deals proceed without delay, while exceptions are quickly reviewed and documented. Maintaining a record of approvals prevents temporary discounts from becoming ongoing expectations.

Governance for exceptions and the deal desk

A deal desk does not need to be complex; for mid-market companies, it can be managed by a single person with a shared queue. Its role is to quickly approve exceptions below the price threshold and monitor patterns. Frequent exceptions from the same account or seller provide valuable insights, indicating either an inappropriate threshold or customer behavior. Making exceptions visible, rather than hidden in individual quotes, enables better oversight. Integrating this check into the quote-to-cash process ensures marginal prices are evaluated at the time of quoting, not after the fact.

Shared definitions across sales, finance, and operations

If sales uses invoice price to measure margin while finance uses pocket price, discussions about marginal price become misaligned. Adopt a single definition—pocket margin—and ensure it is visible to all teams. When sellers see the direct impact of concessions on pocket margin, behavior adjusts without the need for additional directives.

Why does sales compensation drive marginal price leakage?

Here is the uncomfortable part. If you pay sellers on revenue or on volume, you are paying them to lower the marginal price. A rep who closes more by giving a bit more away is doing exactly what the plan rewards. The discount is not a character flaw. It is the comp plan working as designed. We have written before about the reflex to drop the price the moment a customer hesitates, and that reflex is far stronger when commission rides on the close.

Addressing this issue requires adjusting compensation structures, not simply instructing the sales team. Aligning incentives with desired behaviors makes the impact of compensation plans clear.

Compensation basis

What it tends to produce

Revenue only

More discounting to close

Volume only

Margin erosion on incremental deals

Gross margin dollars

Better price discipline

Price realization against the threshold

Strongest alignment with margin

Compensate based on margin, or at minimum, on price realization relative to the threshold. This ensures that sellers who maintain higher margins are rewarded appropriately. Without such incentives, marginal prices will continue to decline in pursuit of quick closes.

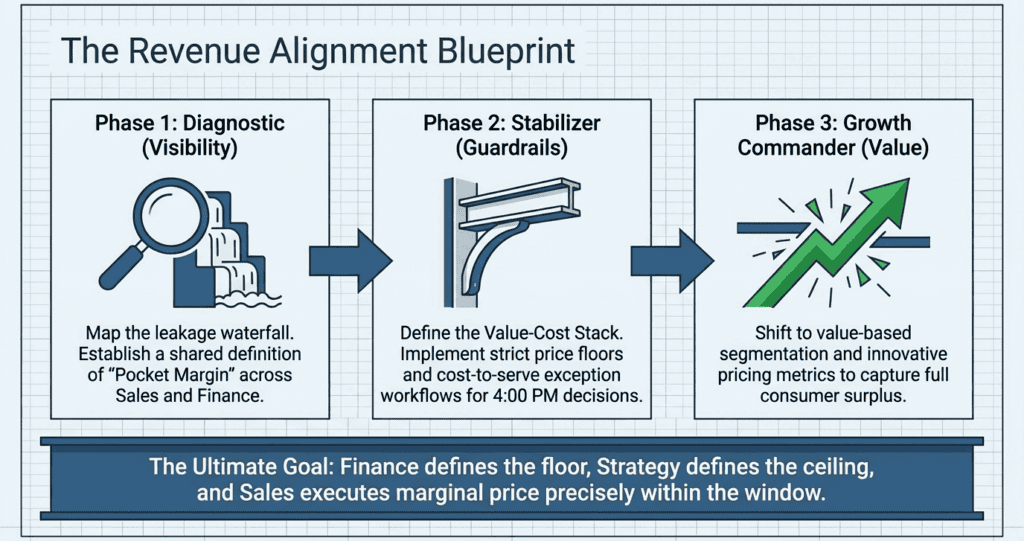

How does Revify’s maturity journey improve marginal price decisions?

A lengthy transformation is not required to address marginal price issues; most improvements appear early. The initial step is an assessment, not a major project. A Profit Diagnostic analyzes the list-to-pocket margin by customer, product, and seller, identifying where marginal prices fall below their thresholds. This process typically reveals key patterns, such as specific territories discounting more heavily, product families priced on outdated costs, or accounts consistently receiving freight concessions.

From there it is sequencing, not heroics. A Margin Stabilizer phase puts the floors, the exception workflow, and a shared pocket-margin definition into how deals get quoted, which is where most of the early recovery lands. A Growth Commander phase sharpens segmentation so the marginal price reflects each segment’s willingness to pay, the price differential that lifts price realization without a list increase. And for companies that would rather not build a pricing department, Managed Services run the function as a virtual pricing team. We cover the mechanics of segmentation in our piece on strategic price customization.

Where are the fast recoveries, and on what timeline?

Improvements in marginal price can be observed within a quarter. The order of implementation is more important than the pace.

First 30 days: find the high-risk exceptions

Begin by identifying where margin leakage occurs. In the first month, review deals with marginal prices significantly below the threshold and identify recurring patterns by account and seller. This stage focuses on diagnosis, not immediate correction, to prioritize areas of concern.

Days 30 to 60: tighten discount control and approvals

Once patterns are identified, establish minimum acceptable prices and implement approval requirements for deals below these thresholds. This step is critical, as it ensures that significant concessions require justification and documentation before approval.

Days 60 to 90: embed governance in daily pricing

By the third month, the price floor, exception queue, and shared margin metrics should be integrated into the quoting process. When new sellers learn the price threshold alongside the product catalog, pricing discipline is fully embedded.

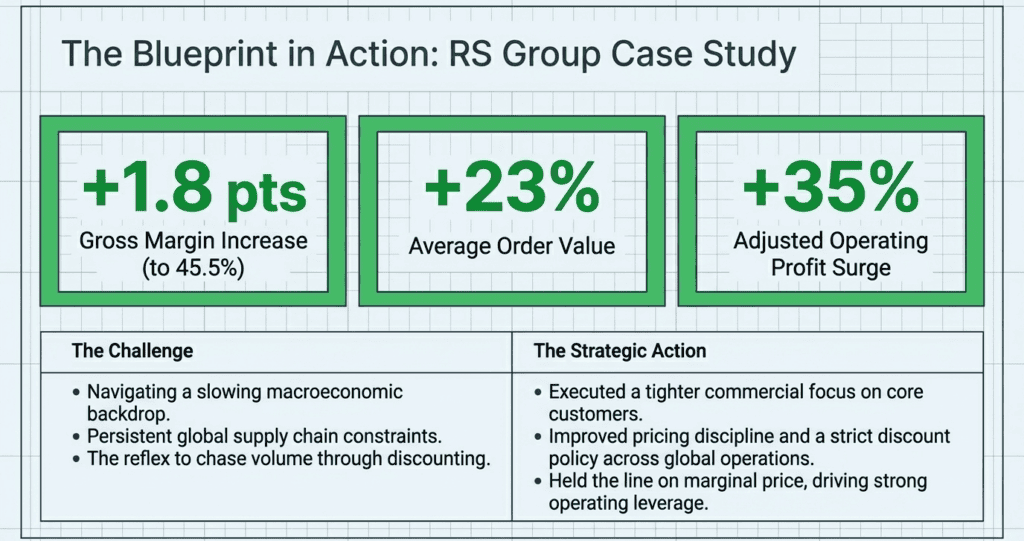

Case: an MRO distributor finds the freight leak

Situation. A regional MRO and industrial-supply distributor kept posting record revenue while gross margin slipped about two points over the year. Its sellers quoted incremental and will-call orders on instinct, and the marginal prices looked fine on the invoice. The pocket margins, after freight and small-order handling, did not.

Actions. A diagnostic broke the waterfall down by seller and account. One pattern stood out, a cluster of mid-size accounts where freight was absorbed on most rush orders and never built back into the price, often on the same low-margin fastener and fitting lines. The team set a marginal price threshold that included freight for those lines and put a quick approval step in front of any quote that fell below it.

Result. Within a quarter, the share of incremental orders quoted below the threshold fell sharply, and pocket margin on that volume recovered most of the lost ground. No list prices changed. The team simply knew where the minimum acceptable price was and quoted it.

Which KPIs show whether marginal price decisions are working?

If only one metric is tracked, prioritize price realization against the established threshold. Monitoring a combination of key indicators reveals whether pricing discipline is being practiced or merely documented.

Price realization by segment and customer type

Pocket price as a percentage of list price, analyzed by segment and customer type, highlights where marginal prices are maintained or declining. Persistent declines in a segment indicate that pricing controls are either being ignored or are improperly set.

Exception rate, approval cycle time, and discount leakage

Monitor the frequency of deals falling below the threshold, approval turnaround times, and the margin impact of approved exceptions. Slow approval processes encourage sellers to bypass controls, and an increase in exceptions with delayed approvals signals a breakdown in pricing discipline.

How well each seller holds the marginal price

Aggregate performance data by seller to identify who secures incremental volume while maintaining marginal price and who relies on margin concessions. This visibility supports targeted coaching and provides evidence for compensation discussions.

What are the common mistakes to avoid?

Several common errors frequently arise when teams begin managing the marginal price.

Setting incremental deal prices based solely on marginal cost. While cost establishes the minimum, cost to serve, and target margin determine the appropriate price.

Assuming any deal priced above variable cost is beneficial. If marginal prices are too low, the overall margin mix deteriorates over time.

Accidentally pricing near marginal cost rather than doing so intentionally. Low prices are appropriate when justified by capacity or inventory needs and have a defined end date. Otherwise, they represent margin leakage.

Relying solely on the seller’s discretion because individual deals seem minor. It is the cumulative effect across many deals that erodes margin.

Frequently asked questions

What are examples of marginal cost?

The cost of making or moving one more unit. Raw materials and components for that unit, the energy to run the line, packaging, and the freight and handling for that incremental order. Rent and salaried overhead do not count because they do not change with each additional unit produced.

How do you find the marginal price?

Start at the marginal cost floor, add the cost to serve that specific deal, then add the incremental margin you want. The marginal price is the number you actually quote on the next unit or order. If it only clears the raw variable cost, it is too low.

Is it ever right to price at marginal cost?

Yes, deliberately and for a defined window. Excess capacity, a perishable backhaul lane, a strategic first order, or aging inventory can each justify a marginal price close to marginal cost. The discipline is to choose it for a stated reason with an end date, not to back into it because a seller wanted the deal.

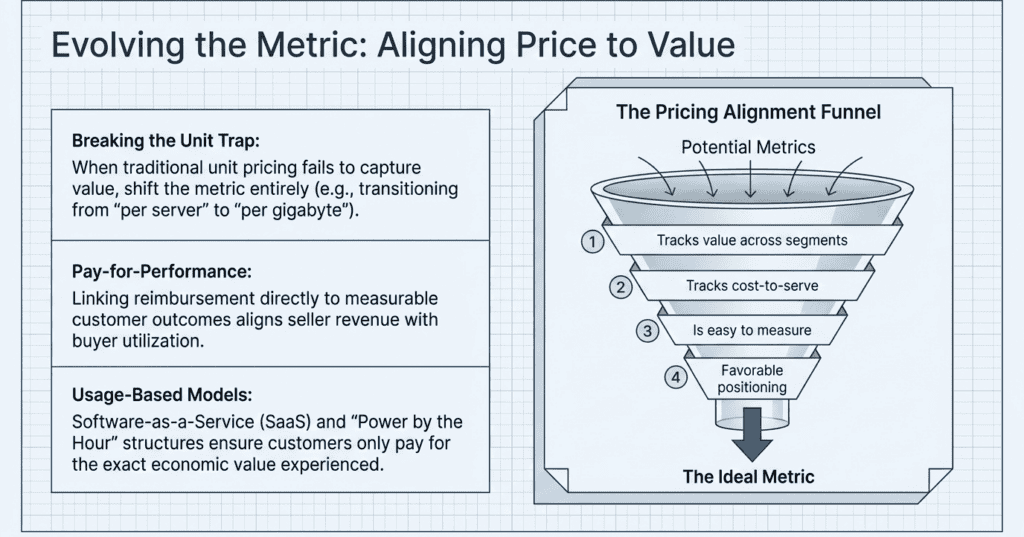

What is marginal value pricing?

Setting the price of the incremental unit against the value the buyer gets from it rather than against your cost. It matters most where willingness to pay varies by segment, which is exactly where a flat marginal price leaves money on the table.

What is the formula for marginal cost?

Marginal cost equals the change in total cost divided by the change in quantity, written MC = ΔTC / ΔQ. It is the cost of the next unit, and it sets the floor that your marginal price must clear.

Is marginal cost the same as price?

No. Marginal cost is the cost of the next unit. The marginal price is what you charge for it. Quoting at or near marginal cost can win the order and still result in a loss of margin once the cost to serve and the target margin are accounted for.

What is a marginal example in pricing?

A spot order for a little extra volume from an existing account. Taking it at a thinner price or holding the line is a marginal decision, and how you price that one order, repeated across a quarter, is what moves the margin line.

Start Your Profit Diagnostic. Revify maps where your marginal price decisions are leaking margin, then install the thresholds and tracking to stop it. See the leak before it shows up in the quarterly numbers.

About the author

Enrico SieniPricing & Revenue Growth Leader, Revify Analytics

Enrico Sieni has spent more than two decades leading pricing and revenue growth for manufacturers and distributors. He has built and run three pricing teams from the ground up, which is part of why he is convinced most mid-market companies do not need one of their own. At Revify Analytics he helps these companies install the discipline, governance, and seller-level tracking that turn price realization from a once-a-year surprise into a number they manage every week. He writes about the practical side of pricing: what actually moves margin, and what only sounds good in a deck.

By Enrico Sieni ·Revify Analytics ·2026-06-17 ·~13 min read Channel pricing is the discipline of setting, governing, and tracking what each route to market actually pays you, from list price

By Enrico Sieni · Revify Analytics · June 10, 2026 · ~12 min read You can improve price realization without hiring a dedicated pricing team. Results come from disciplined processes:

How mid-market manufacturers and distributors move from textbook elasticity to discount discipline, measurement rigor, and durable margin lift. By Enrico Sieni · Revify Analytics · Published May 27, 2026 ·